“Some of these affordable housing companies saw a good run-up in their stock prices because there was an emphasis on rural housing schemes in the budget,” Dhaval Gada, fund manager at DSP Mutual Fund, told Mint. “The buzz around Bajaj (Housing Finance’s) IPO has also caused some sharp movement in their prices, particularly for the more comparable big players like PNB (Housing Finance).”

Strong demand visibility, substantial government support and high return on assets (ROA) have provided significant tailwinds to these companies. In the past six months, stocks of the top pure-play affordable housing financiers – Aadhar Housing Finance, Aavas Financiers and Home First Finance Co. India have posted an average return of 34%. Only Aptus Value Housing Finance lost about 6% in this period as it reported a relatively lower velocity of disbursements and poorer quality of assets in the quarter ended June.

However, market participants remain bullish on affordable housing because they see it as a burgeoning sector with enough room for a variety of players. The market has already handsomely rewarded those venturing into this segment. A case in point – PNB Housing Finance.

PNB Housing’s stock has generated 50% returns in the past six months, the highest of all housing finance companies. During Q1 of FY25, 32% of the company’s incremental disbursements were towards the affordable housing and emerging market segments. The company plans to increase this share to 40-45% by the end of this fiscal.

“There was an overhang of some private equity block deals which were due for PNB (Housing). Now that those are done, its stock price is catching up with the rest of the players in the affordable space,” Gada said.

As part of its broader push into the retail loan segment, the housing financier is targeting an affordable housing portfolio of ₹5,000 crore by FY25 and ₹15,000 crore by FY27.

In contrast, shares of Can Fin Homes and LIC Housing Finance, which are yet to make meaningful entries into the affordable housing segment, have offered an average return of 10% in the past six months.

Profitable model

The affordable housing segment is lucrative for housing financiers because these loans typically have high rates of interest, which generate higher ROAs for them.

“The lending rate (in the affordable housing segment) is around 12-13% on average, unlike that in the prime segment where the rates are more competitive at around 8-11%,” Anusha Raheja, research analyst at Dalal & Broacha Stock Broking, told Mint. “Since the ROA in this business is better than the prime segment, valuations of the companies in the affordable housing space are also better.”

Affordable housing loans are written at a more grassroot level. They involve physical underwriting and collection processes, which increase operating costs. A riskier borrower profile and lower quality of collateral relative to the prime segment increases funding costs as well.

As a result, affordable housing financiers charge higher interest on their loans. However, several subsidised refinancing schemes from the National Housing Bank ease their funding costs, resulting in wider interest margins and hence a higher ROA for them.

Moreover, the government’s credit-linked subsidy scheme reduces borrowers’ liabilities by subsidising the principal portions of their loans. This reduces the credit risk for lenders, making the overall business model profitable for them.

“The key reason why PNB (Housing) has significantly ramped up its affordable housing loan distribution is because it provides better profitability, as the model comes with higher ROAs by design,” Gada said. “Also, it helps them to diversify their cohort of customers.”

Also Read: Bajaj Housing will not need more capital in the next few years: Sanjiv Bajaj

With renewed impetus from the government to offer affordable housing to the poor, market participants said the growth opportunities in this segment are higher than in the prime segment. The Union Government announced the Pradhan Mantri Awas Yojna (PMAY) 2.0 scheme in its 2025 Budget to provide 20 million additional houses in the next five years.

“Anybody catering to the EWS (economically weaker section) and LIG (low-income group) segment has great tailwinds in the form of government support through PMAY 2.0,” the chief financial officer of a large housing finance company told Mint on condition of anonymity. “Demand in the market is very strong. So, there is enough headroom for this industry to grow. Moreover, with (interest) rate cuts on the cards, these loans stand to do better as (net interest) margins are still very good. But that bump will be offset within a span of four to six months of the cuts.”

Strategic difference

Even though the affordable housing segment is a profitable business model, it is not the only one in the housing finance space. The non-housing corporate or builder loan segment is another high-yielding space in which Bajaj Housing Finance has a strong footing.

“Companies operating in super prime or prime segments operate on thin margins. To complement that, they get into the corporate or affordable housing segment,” the CFO cited earlier said. “Since both these segments generate relatively higher yields, they help in balancing the profitability.”

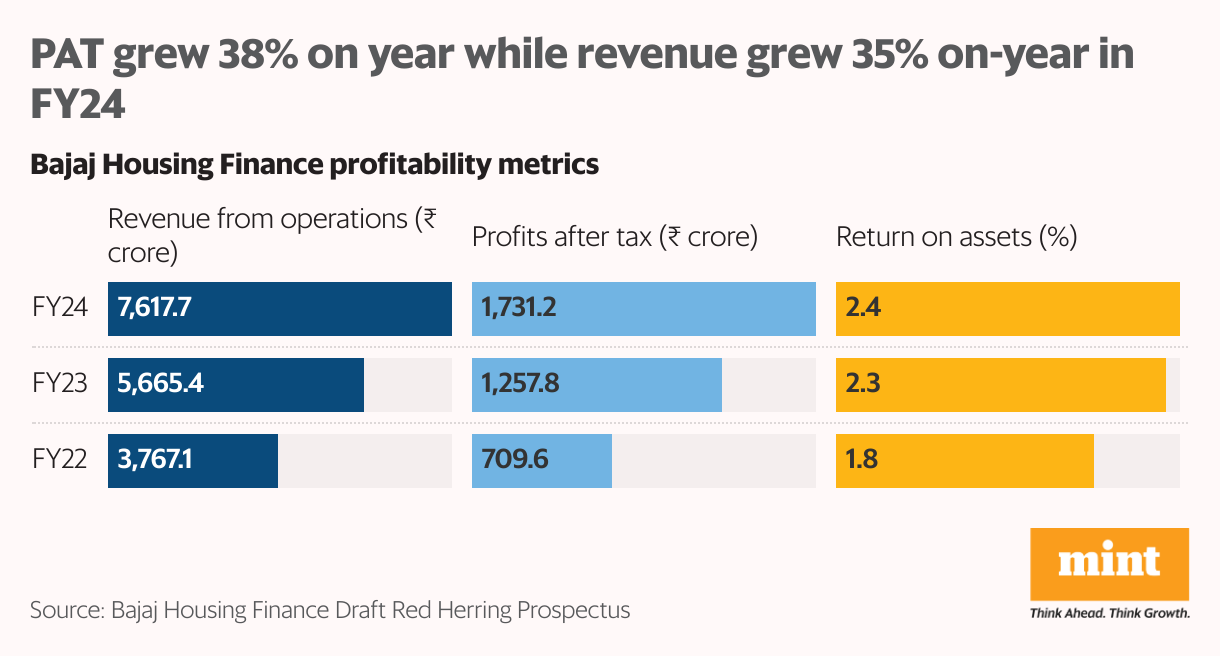

With total assets under management at a little over ₹97,000 crore as of Q1 FY25, Bajaj Housing Finance is one of the largest housing financiers in the country. The company’s revenue grew 35% on-year to ₹7,617 crore while net profit increased 38% to ₹1,731 crore in FY24, according to the draft red herring prospectus filed by the company for its IPO.

Also Read: Govt to announce norms, widened income criteria for housing help this month

“Bajaj (Housing) is comfortable with their strategy. They are one of the largest players and their growth and asset quality has also been better than the rest,” Raheja said. “Hence, they are being valued at a higher multiple even though they are not in the affordable housing segment.”

The company’s stocks already fetch an about 80% premium in the grey market ahead of its listing, indicating a strong demand for its IPO. The housing financier has set a price band of ₹66-70 per share.

“Corporate and affordable are both very different strategies. Whatever strategy they have adopted, they must execute them well,” the CFO quoted earlier said. “Their (Bajaj Housing’s) multiple is not very different from that of affordable housing companies. They just have to be at the top of their game.”