On the face of it, revenues expanded 8% on a year-on-year basis, the fastest in three quarters, but profit growth slacked off to 31%, the slowest in 2023-24 so far. But on the flip side, thanks to struggling rural demand, that revenue growth is highly subdued as compared to what it was just four quarters ago (18%); yet, profits growth is shining in double digits on account of reduced input cost pressure.

Meanwhile, India Inc. finally came out of the shadow of the vibrant fortunes of the country’s banking and financial sector, which had been riding on healthy business performance and asset quality so far, but were no longer the primary driver of the profit growth in the December quarter, showed a Mint analysis of the earnings of 3,478 BSE-listed companies. Excluding banking, financial services and insurance (BFSI) firms, total revenue growth returned to positive territory (3.4%) after two consecutive declines, and profits swelled by nearly 43%.

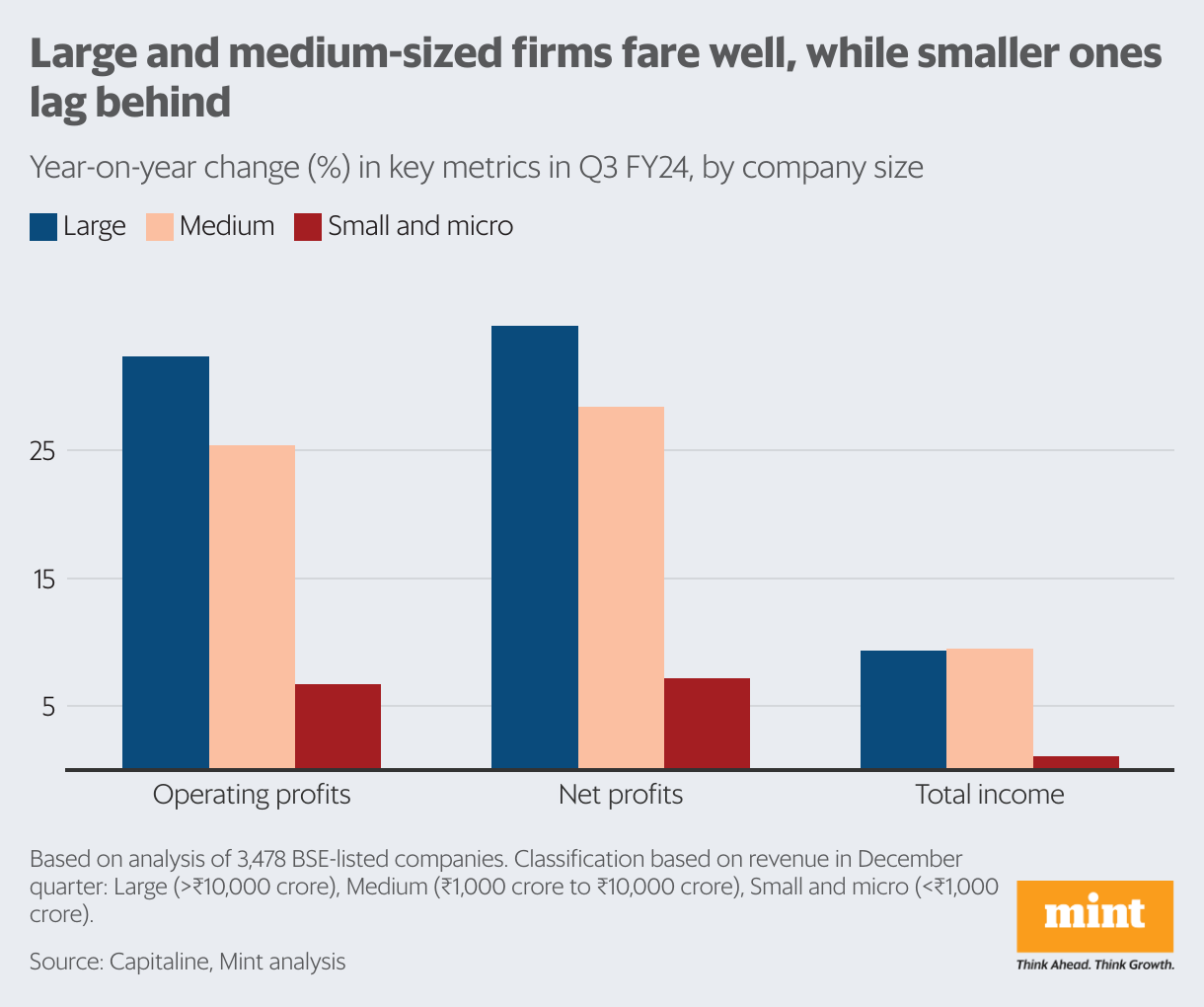

Sequentially, revenues rose 3.6%, a three-quarter high, while profits shrank marginally, largely on account of smaller companies in the sample, whose profits shrank 38%. Even on a year-on-year basis, small businesses’ profit growth lagged larger firms.

Size was not the only factor dictating the hits and misses this quarter. Across sectors, too, the performance was not uniform, with rural demand remaining a major pressure point, a Bank of Baroda report dated 22 February pointed out.

Banking in spotlight

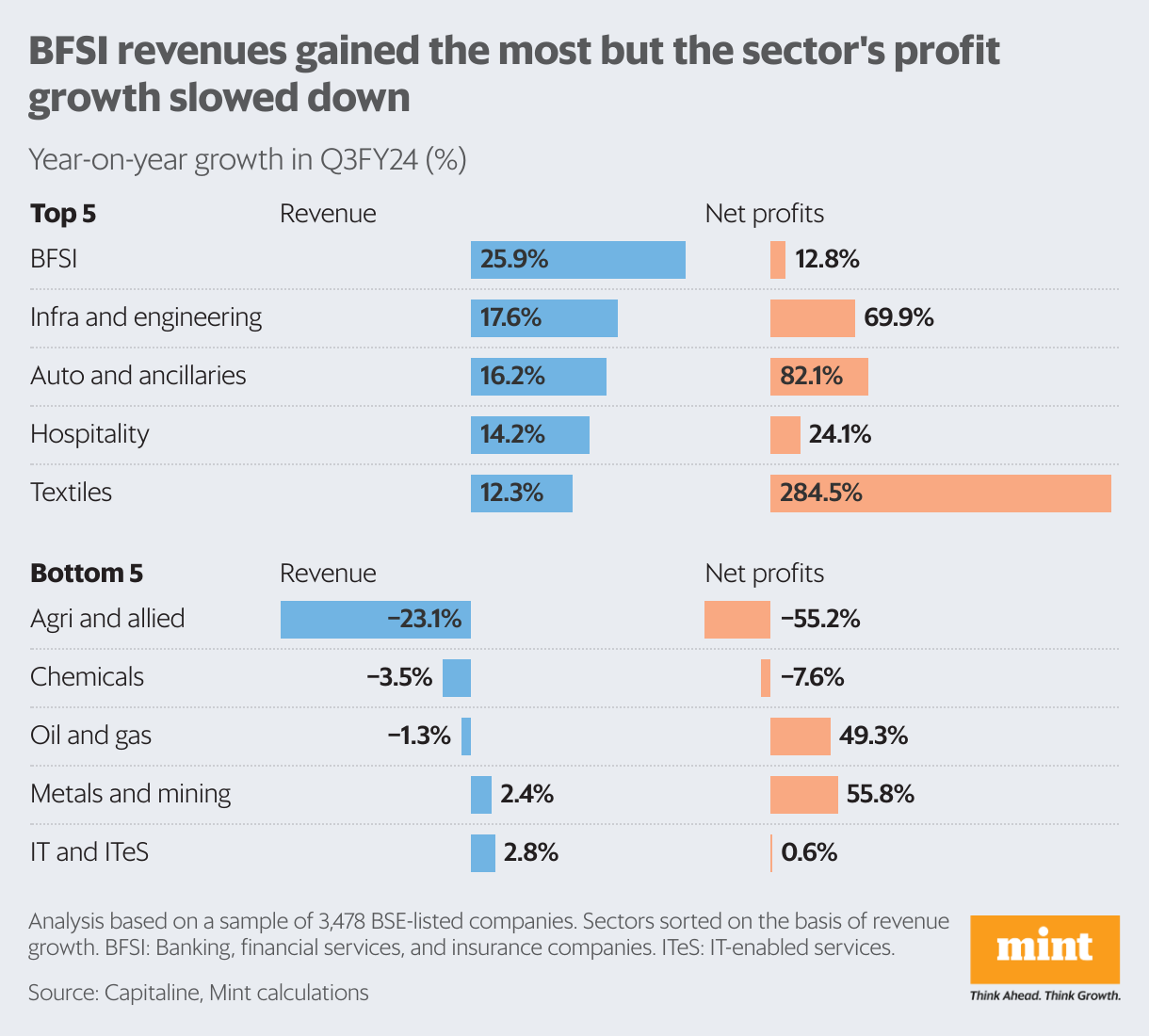

The overall earnings show was impressive, but surely not broad-based. As many as 11 of the 18 key sectors covered in the analysis showed some slowdown in their net profit growth. Among them was the BFSI sector, which had largely done the heavy-lifting for corporate India earnings in recent quarters. The sector’s profits rose 12.8% from a year ago, against a 31% growth in the September quarter. Sequentially, the sector witnessed a contraction in net profits.

“With the exception of a few public sector banks, the majority of banks saw their margins remain flat or slightly decline,” said Palka Arora Chopra, director at Master Capital Services Ltd.

However, the sector remained a leader in terms of revenue growth (25.9%), followed by infrastructure and engineering (17.6%), auto (16.2%), hospitality (14.2%) and textiles sector (12.3%). For nine of the 18 sectors, revenue growth exceeded the aggregate rate of 8.4%.

Relief on the way?

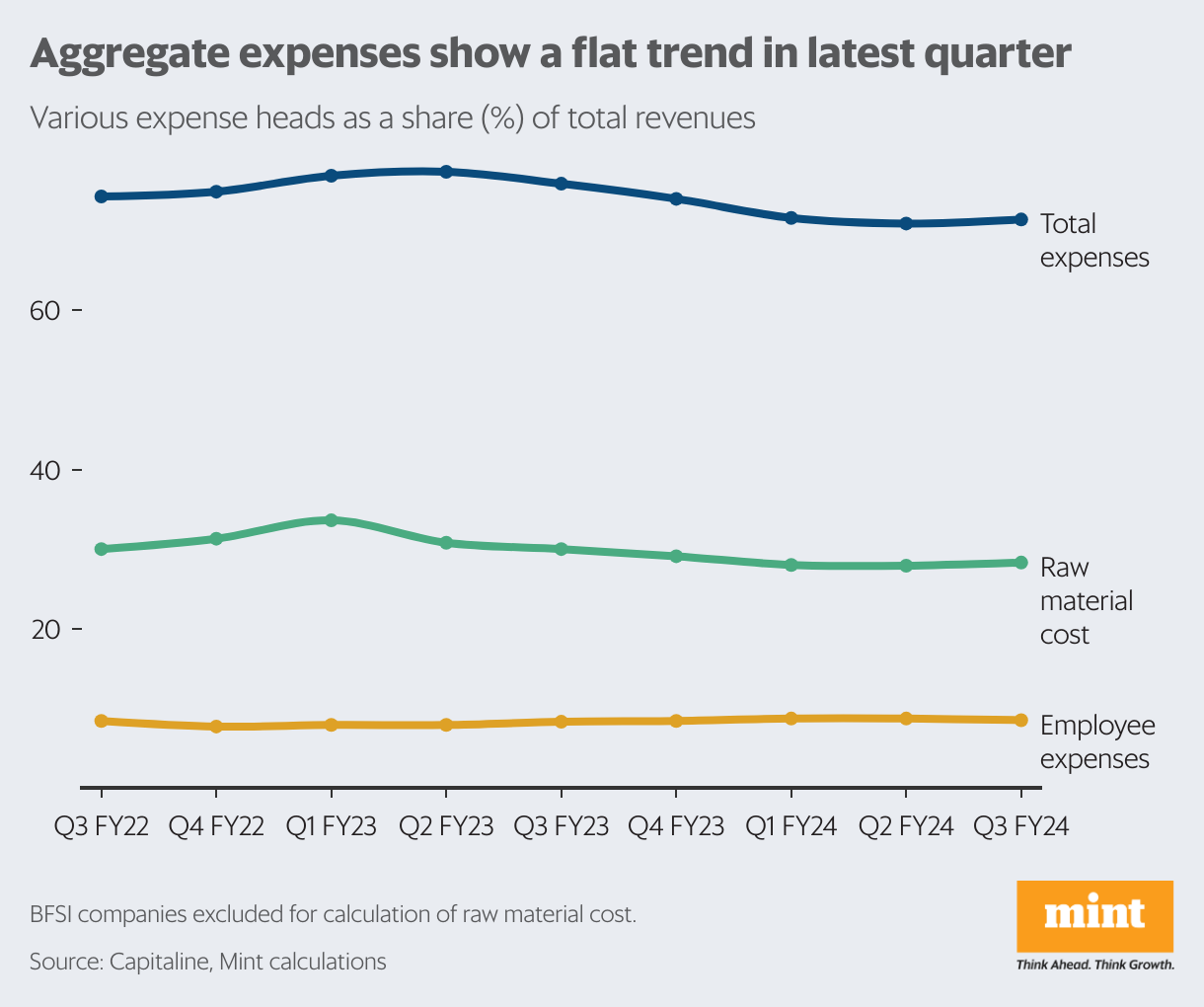

Not too long ago, businesses faced the terror of high expenses—both on account of raw materials and employee salaries. Much to their relief, the pressure has tapered down. In the December quarter, total expenditure was up only 2% from a year ago, with the pace stable for some time. As a share of revenue, aggregate expenses for the sample stood at 71.4%, roughly unmoved for three quarters.

The raw materials head has also been coming under control since a high of 33.6% as a share of revenues in April-June 2022. In the last four quarters, it has come down from 30% to 28.3% (with only a marginal rise in the December quarter). Employee costs were 8.5% of revenues, marginally down from the preceding two quarters but slightly higher compared to the same quarter a year ago.

“With input prices abating, profit margins have seen a sharp uptick…contributing to higher profits,” the Bank of Baroda report said.

Margins risk

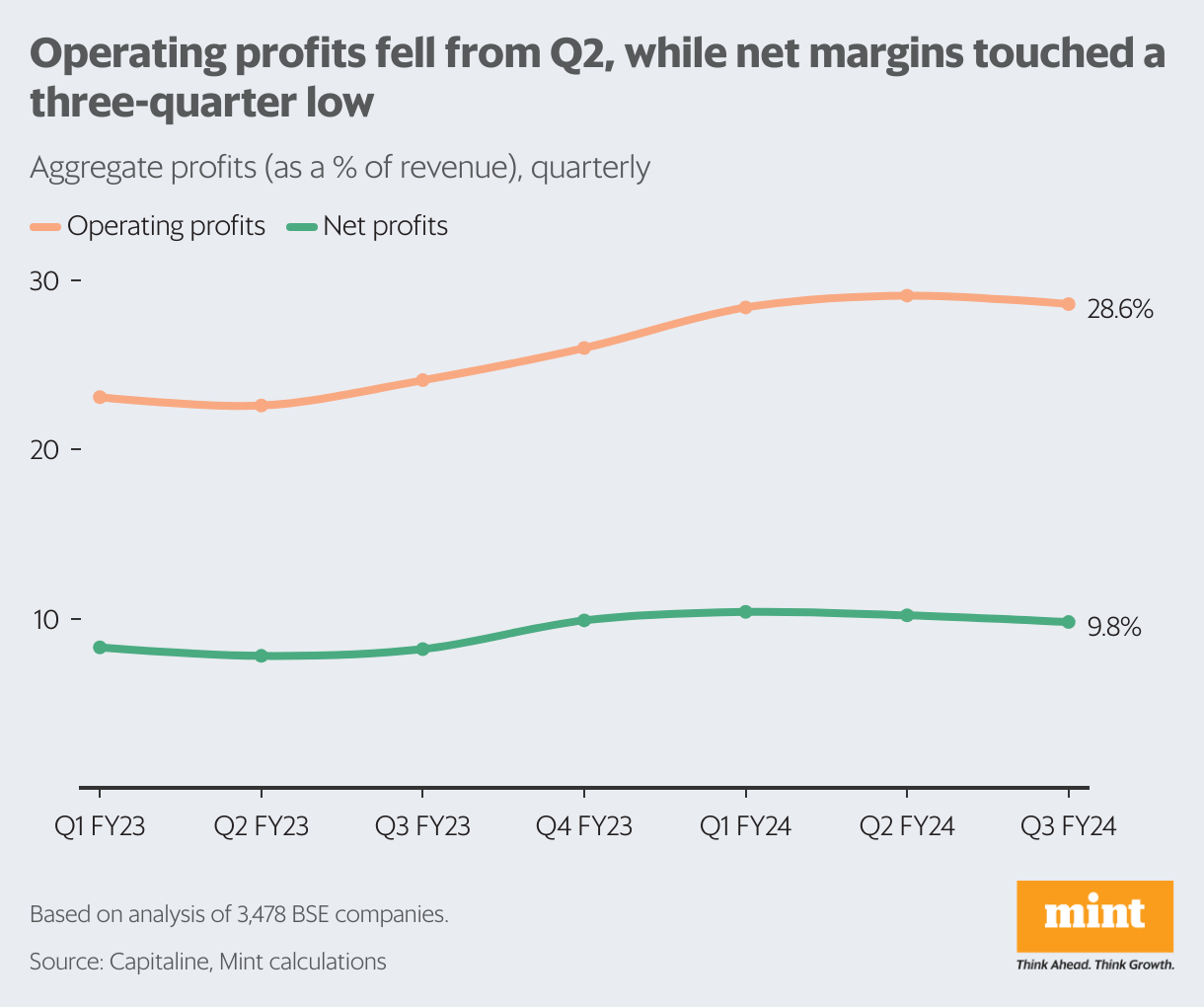

Aggregate operating margins remained strong, rising from 24.1% a year ago to 28.6% in the December quarter. However, there was a 57-basis-point dip on a quarter-on-quarter basis. Net profit margins—or net profits as a share of revenue—moved in tandem, seeing a dip in the last two quarters, even as it rose on a year-on-year basis.

The signs of stability on margins could change in the coming months. “The next few quarters may remain volatile or a mixed bag as freight costs are on a rise due to the Red Sea crisis, affecting some of the input cost and margin,” said Mukesh Kochar, national head of wealth at AUM Capital.

On the positive side, companies could also expect a lift from increased consumption demand, especially in urban areas, in election season, Kochar said. However, that’s not to say that the rural demand factor is out of the woods: analysts will closely watch the recovery on that front.