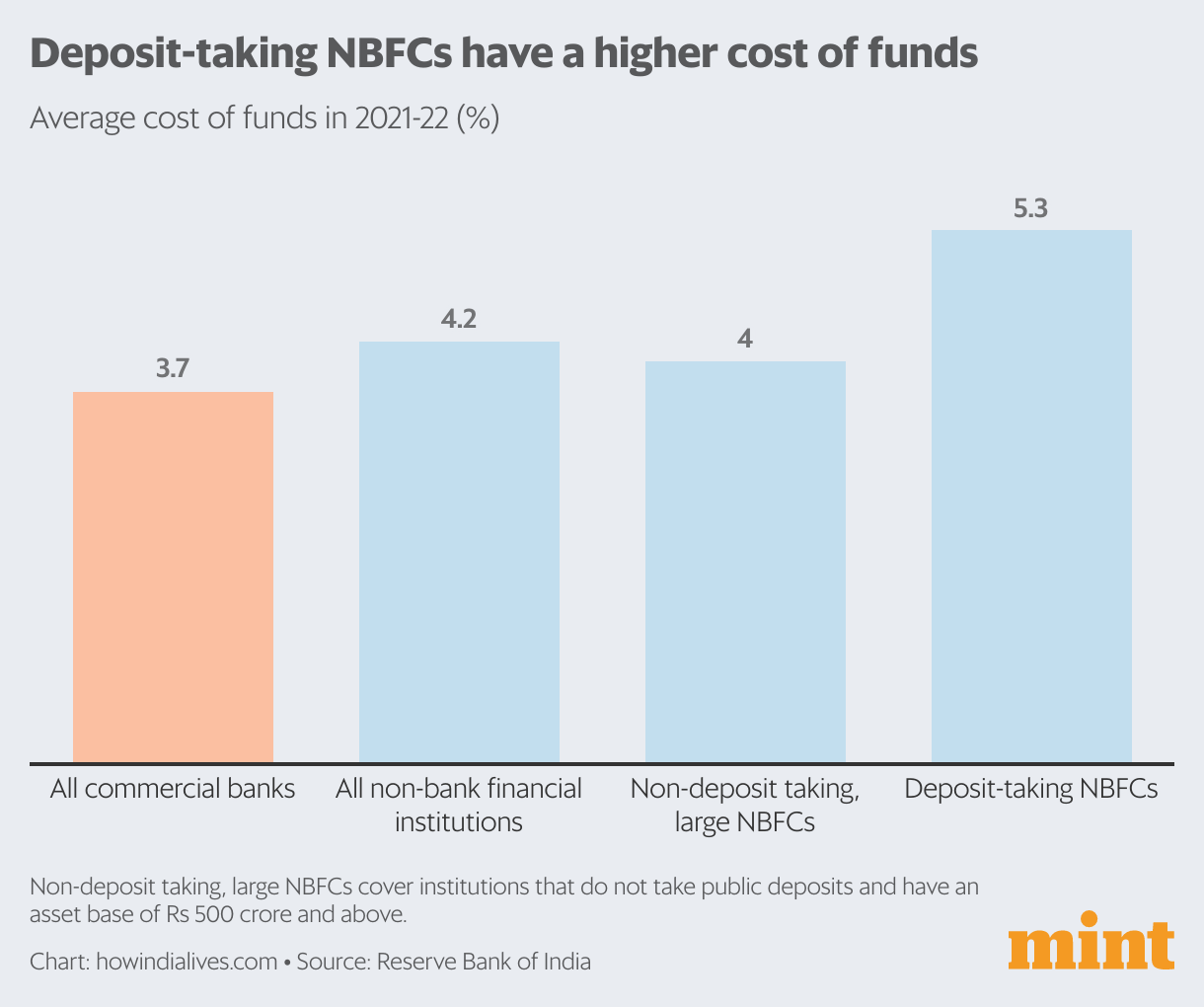

A major reason for the long-awaited merger of HDFC and HDFC Bank was costs. In the Indian financial system, only banks can raise funds from the public through current accounts and savings accounts, on which they pay either no or very low interest. Such deposits accounted for 44% of HDFC Bank’s fund base in 2022-23. In contrast, non-bank financial companies (NBFCs) such as the erstwhile HDFC can only raise term deposits from the public, that too typically at higher interest rates than banks. Thus, the average cost of funds for HDFC was much higher than that for HDFC Bank.

Yet, this relative disadvantage on cost of funds alone doesn’t dismiss a case to be an NBFC. The NBFC sector, as a whole, is varied in terms of size, ownership and business profile. Broadly, NBFCs are classified into those that are allowed to raise deposits from the public (like HDFC) and those that are not.

The Reserve Bank of India, which regulates NBFCs, further splits the second category into institutions whose asset base exceeds ₹500 crore, which it considers ‘systemically important’. This category includes several large government-backed companies (such as Power Finance Corporation), which account for 45% of assets in this category. Their government-owned status means they can raise funds at a lower cost, thus pulling down the cost of funds for the NBFC sector as a whole. In contrast, NBFCs allowed to raise public deposits account for 14% of the sector and their cost of funds is typically higher than that of banks.

Margin boost

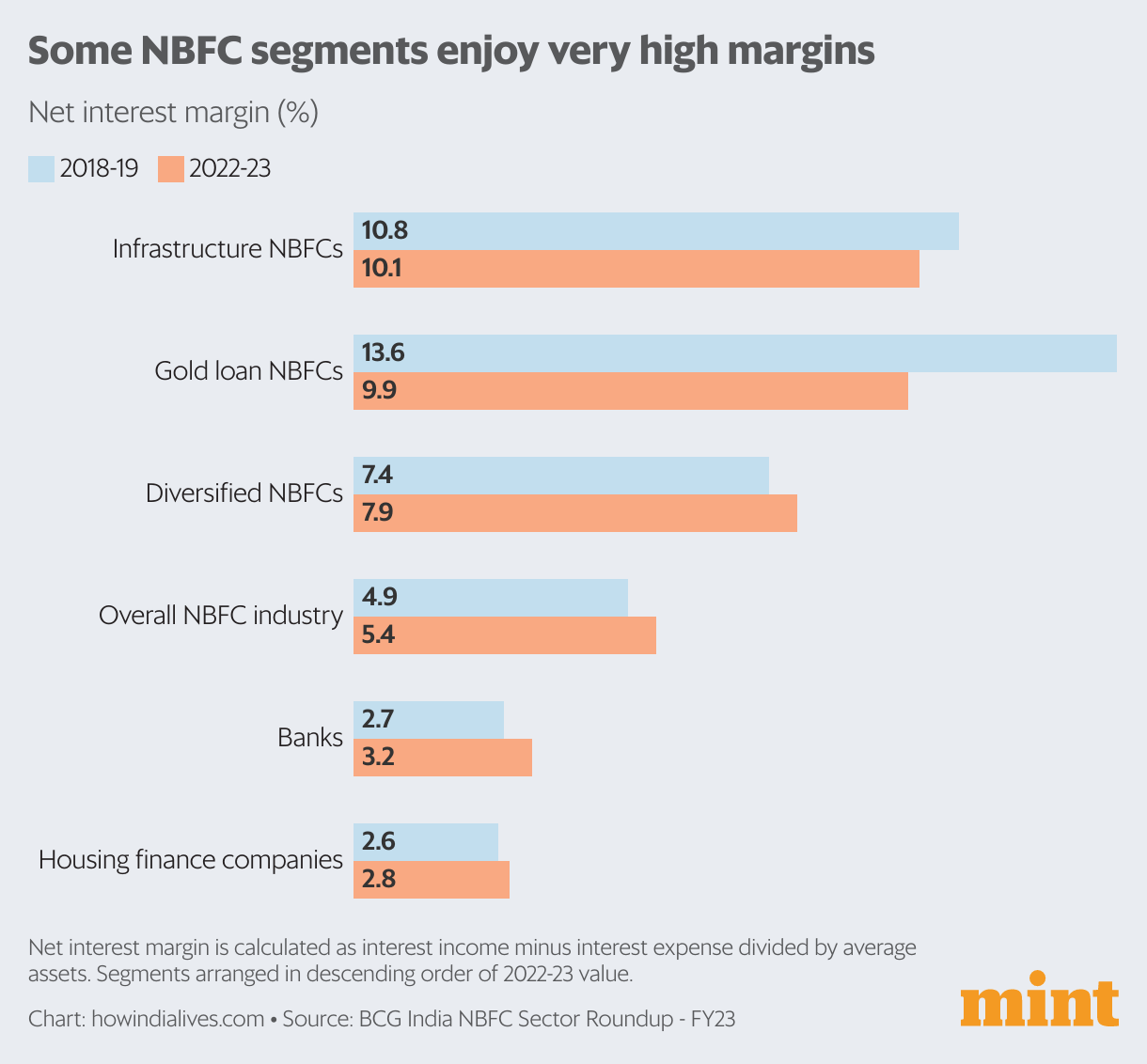

The business case for NBFCs comes from margins. As a whole, margins of NBFCs tend to be much higher than that of banks. This is because NBFCs are more focused on higher-margin retail loans such as gold loans, vehicle loans and microfinance. While the share of retail loans in total loans for both groups is roughly the same (around 28% in 2022-23), banks tend to have a much larger share of lower-margin home loans in their loan book. Excluding home loans, the share of retail loans in overall loans for NBFCs was 27.7% versus 13.8% for banks.

Thus, as a whole, the net interest margin for NBFCs was 2.2 percentage points higher than for banks in 2022-23. Among NBFC segments, infrastructure loan and gold loan companies had the highest margins. The exceptions in the NBFC sector were housing finance companies, the category to which HDFC belonged. Due to intense competition from banks, margins for housing finance institutions were lower than for banks.

Market approval

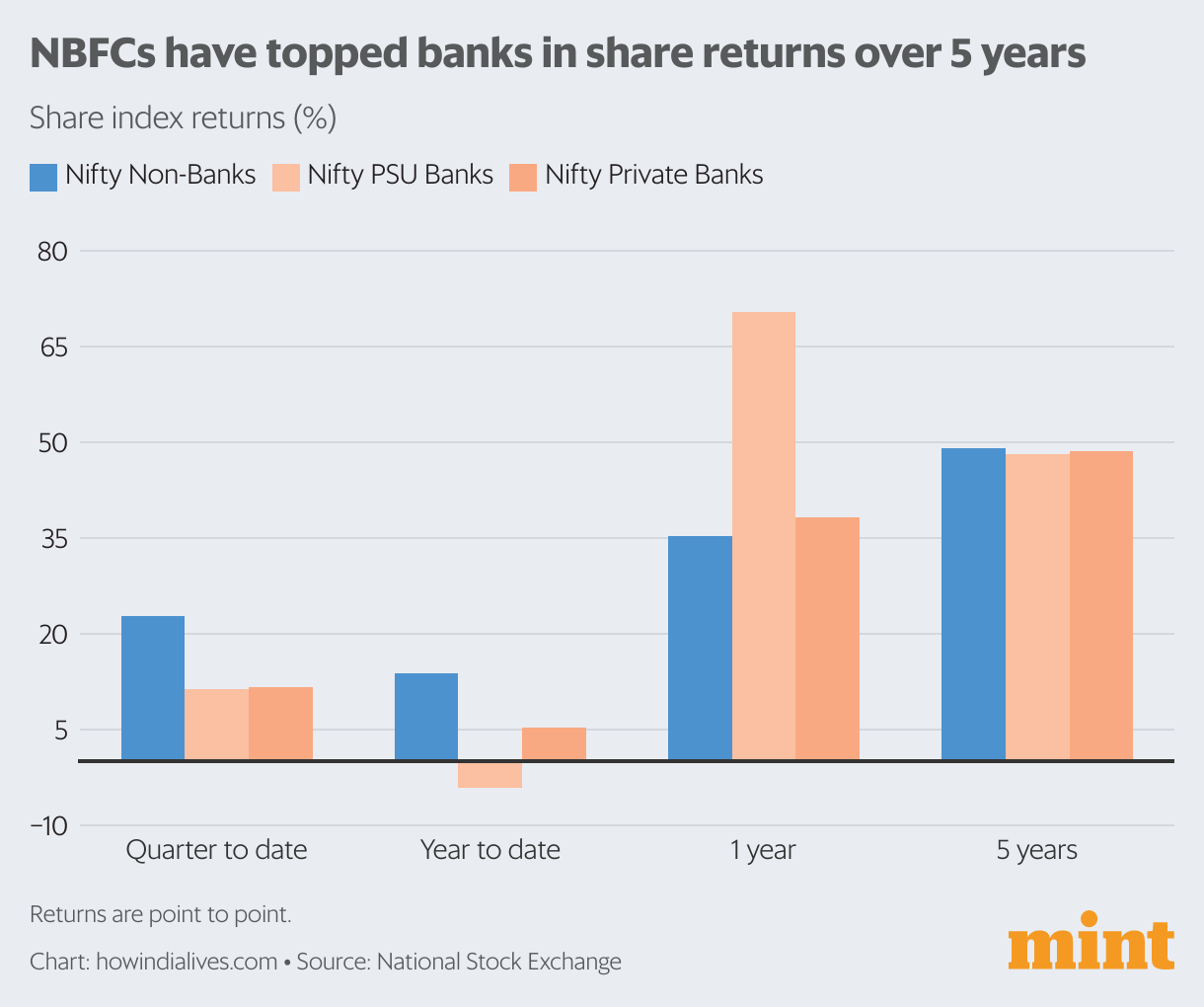

NBFCs that are more retail-oriented, especially in higher-margin segments, have done well on the growth front in the past few years. Thus, over a five-year period, share performance of the NBFC set has topped both private banks and public sector banks. Over a one-year period, while stock market performance for the financial sector as a whole has been strong, NBFCs have trailed banks, especially public sector banks, whose stocks were on a tear till the last quarter.

Valuations of large NBFCs such as Bajaj Finance and Cholamandalam Finance top even that for leading banks. According to a review of the NBFC sector by the Boston Consulting Group, as of end-May, Bajaj and Cholamandalam had a price-to-book ratio of 8.2 and 6, respectively. By comparison, it was 3.2 for HDFC Bank, 3.6 for the erstwhile HDFC and 1.7 for SBI. According to BCG, the so-called ‘diversified’ NBFCs, who are active in several sectors, commanded higher valuations.

Home-loan hurdle

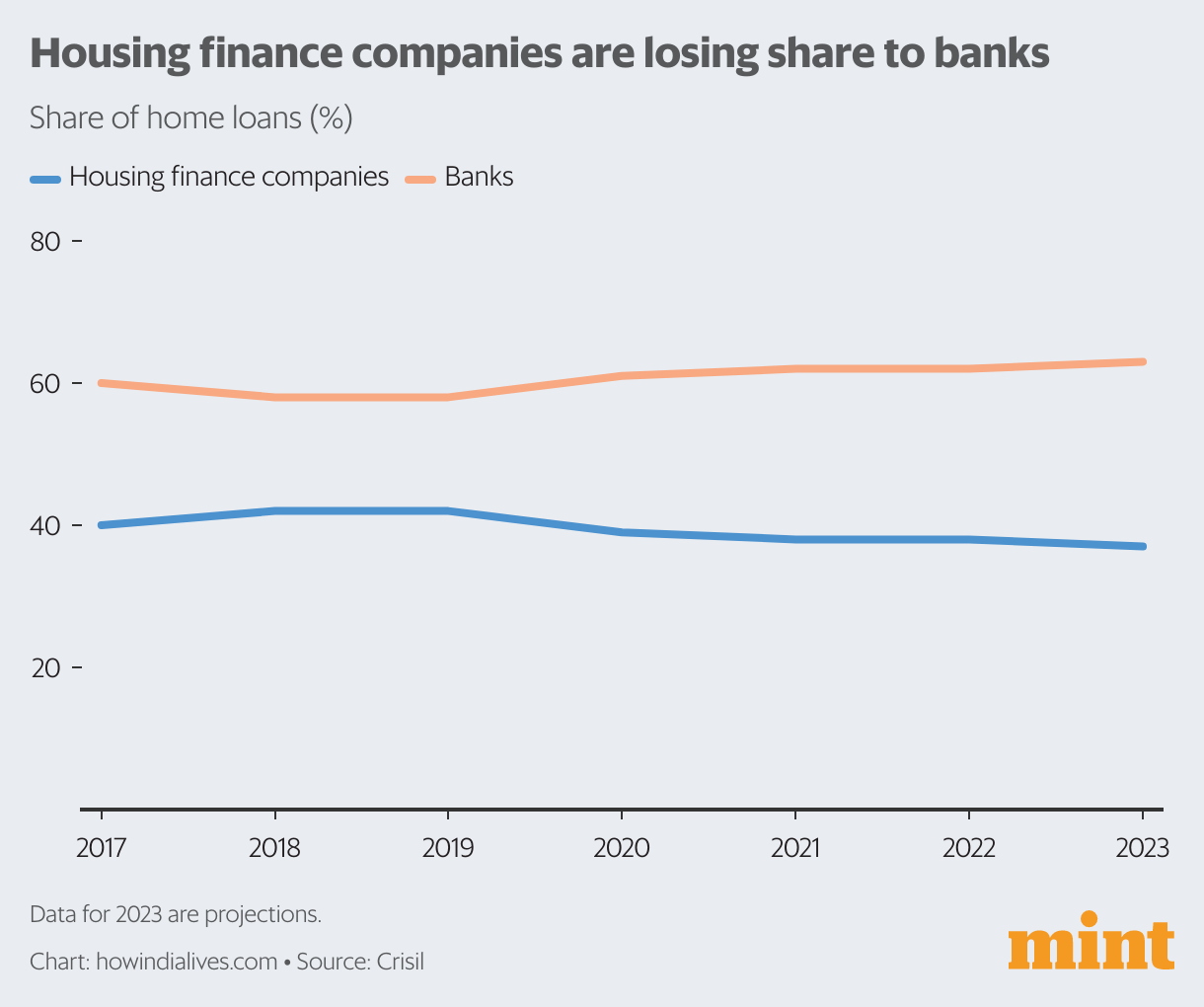

The HDFC merger also puts the spotlight on housing finance companies (HFCs). Given the intense competition from banks and low margins in housing finance, do HFCs have a future? While the post-covid recovery led to strong home-loan growth for NBFCs active in the sector, a Crisil report last year argued that HFCs were expected to continue losing home-loan market share to banks amid stiff competition. “While access to funding is not a big challenge for most HFCs, competitive borrowing cost is crucial versus banks, which benefit from low-cost deposit funding,” the report said.

Between 2019 and 2022,HFCs have lost 4 percentage points of market share to banks, who now account for 62% of the home-loan market. “This trend is unlikely to reverse in the near term,” Crisil notes. While NBFCs oriented around home loans will be challenged, the business case for the more diversified NBFCs remains.

www.howindialives.comis a database and search engine for public data