It’s a new year and there are new hopes. Will 2024 deliver new highs to the Indian stock markets? Towards the fag end of December, key benchmark indices, the Nifty50 and S&P BSE Sensex, scaled new peaks. This was driven by positive domestic as well as global newsflow.

For one, the Reserve Bank of India raised its gross domestic product growth forecast for FY2024 to 7% from 6.5% after September-quarter (Q2FY24) growth came in better than expected. Anticipation of interest rate cuts by the US Federal Reserve also fuelled sentiments. As such, liquidity influx by both domestic and foreign institutional investors into Indian stocks has been robust.

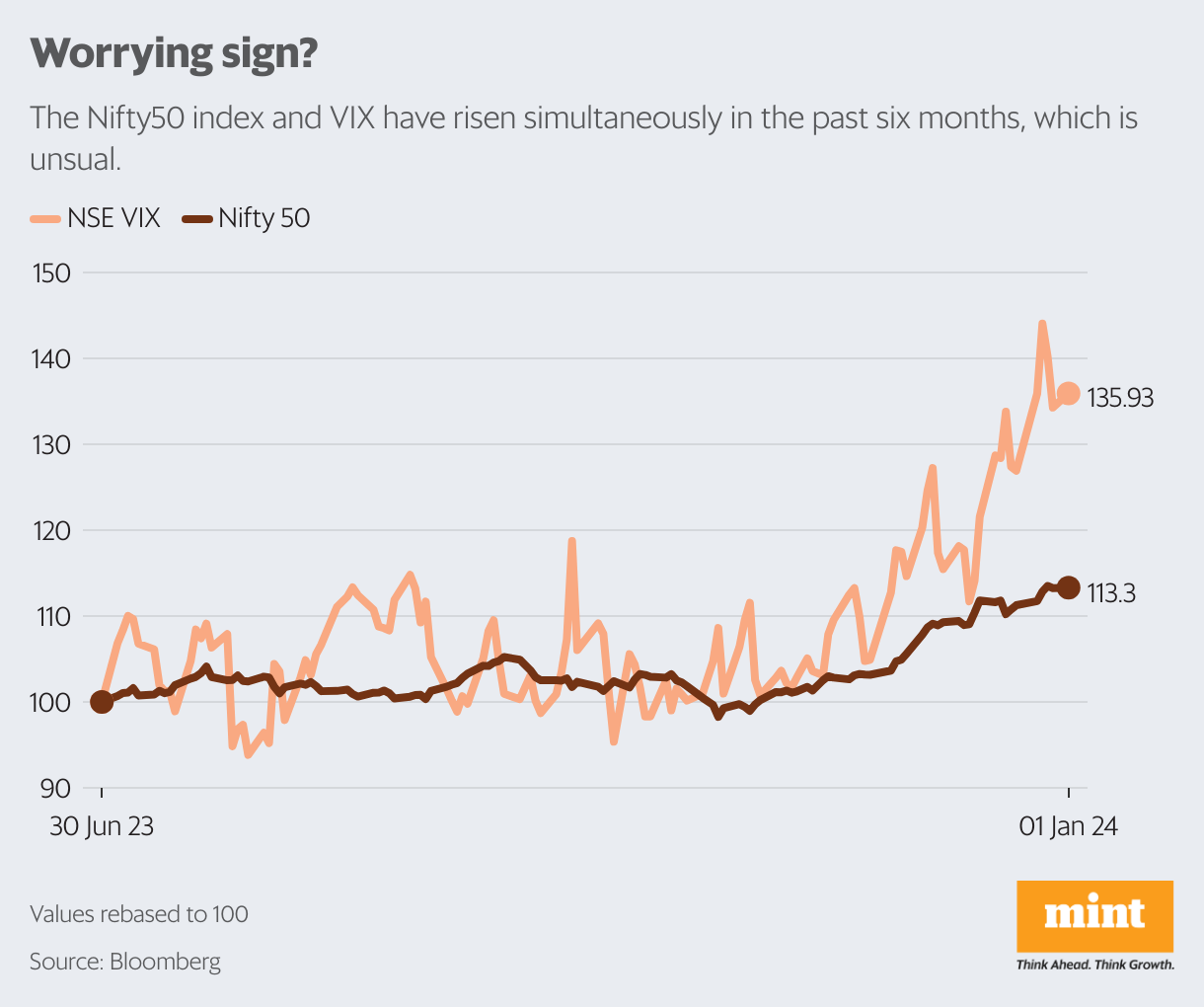

Amid the oozing optimism, the fear gauge that is the NSE volatility index (VIX) has risen by 35% in the previous six months. Theoretically, the movements in VIX and benchmark indices are inversely related. Simply put, this means that the Street is currently fixated on positives, turning a blind eye towards potential threats.

This is despite India’s expensive valuations. The MSCI India index is trading at a one-year forward multiple of nearly 22 times, a glaring premium to the MSCI Asia Ex-Japan and MSCI EM Index, show Bloomberg data–thus leaving no room for disappointment. Particular hotspots are pricey Indian midcap and smallcap stocks, which beat large caps massively in 2023.

Another positive factor was the outcome of recent state elections in favour of the Bharatiya Janata Party, which administers the Union government. It has soothed investors’ worries about policy and administrative uncertainty as the market braces for the general election this year, likely in April or May. But despite increased investor confidence about continued political stability, predicting the outcome of the general election is tricky.

“An analysis of the past five general elections (which are more relevant given incumbent governments have served full 5-year terms), indicates that markets approach the elections with optimism. Nifty index rose an average 13% over the 6-month period leading up to the elections,” Standard Chartered said in a report.

This can be attributed to a pick-up in pre-election spending and populist measures, both of which are positive for consumption demand. Although, unless the actual event of the 2024 general election is out of way, a potential event risk remains. “History shows that election outcomes can be unpredictable as sentiments can swing throughout the campaign season,” Standard Chartered said.

In 2024, the US too is slated to have its general election, the outcome of which tends to have global economic repercussions. Despite the global liquidity scenario turning supportive, an unexpected outcome could be a dampener. Plus, geopolitical conflicts are not completely out of the way.

Chinese economic growth can also disappoint. “China is slowing down. This can be a double-edge sword for other developing countries. While on one hand, countries like India are gaining from China+1 strategy, a slowdown in any major economy does have a collateral negative impact on the rest of the world,” BOB Capital Markets said in a report.

Back home, the trajectory of corporate earnings growth and revival of rural demand are key for the consumption theme. Analysts, however, are of the view that election-related developments can overshadow India Inc’s Q4FY24 and Q1FY25 performances. Further, a steep resurgence of Covid cases leading to restricted economic activity would be undesirable.

“In our view, it would be best to enter 2024 with low return expectations from the market,” Kotak Institutional Equities said in a report dated 27 December. The broking firm cautions that the market may conveniently ignore the fact that valuations of most stocks are well above their pre-pandemic levels, while interest rates will likely be higher versus pre-pandemic levels even after potential rate cuts in 2024-25.