NestAway was founded in 2015 and had raised about $110 million from a bevy of marquee investors, including Tiger Global, Ratan Tata-backed UC-RNT Fund and Goldman Sachs. It was valued at nearly $220 million in 2019.

The pandemic, which began in 2020, halted the expansion plans of many co-living startups due to a sharp drop in demand and occupancy. NestAway’s troubles, however, preceded the pandemic. As one of the first movers in India’s shared living ecosystem, the startup’s growth was brisk, attracting early investors to bet on a nascent real estate business. Flush with funds and chasing growth, its losses ballooned. So, after the pandemic hit, when revenues shrank and new money was hard to come by, the startup, which once said it aimed to be the Indian version of Airbnb, didn’t have a choice but to look for a buyer.

Post acquisition, Aurum PropTech took a slew of steps to turn the company around. HelloWorld turned Ebitda (earnings before interest, taxes, depreciation, and amortization) positive in June 2023, while NestAway turned profitable in December. Before that, Nestaway was losing around ₹2.5 crore every month, Jitendra Jagadev, co-founder and chief executive officer (CEO) of HelloWorld and NestAway, said.

View Full Image

HelloWorld, which was operating 7,400 beds pre-acquisition, manages around 15,000 beds today. Nestaway has scaled to 20,000 rental units from 15,000 units.

Jagadev said costs were drastically brought down to improve profitability. And operations were halted in a few cities that were not profitable. “By leveraging technology, operational efficiencies were enhanced, which has significantly reduced people and other direct costs,” he said.

Co-living is the residential version of the co-working model, where companies operate shared living facilities on a monthly rental basis. As per data by Tracxn, there are 119 Indian co-living startups, 68 of which are active.

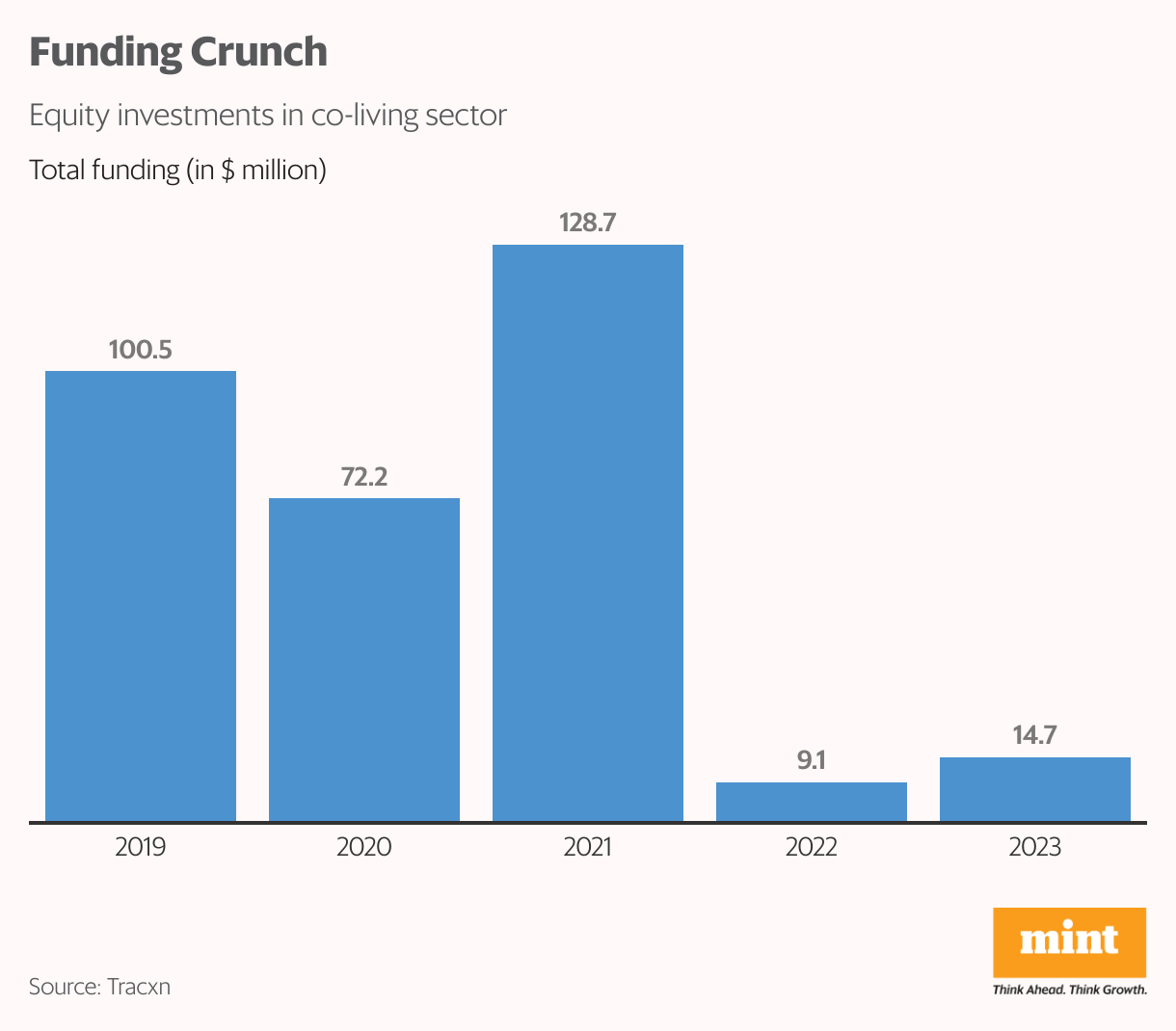

The sector dates back to 2015. It has undergone a sharp churn. To begin with, funding has been hard to come by—it plunged from $128.7 million in 2021 to $14.6 million in 2023.

Many early operators didn’t survive the multiple challenges of an operationally heavy business, fund-raising and occupancy pressure, which led to the basic business model being questioned. The largest and most-funded startup in this space, Stanza Living, is also losing more money than it earns.

Going by data from Tofler, Stanza Living, which provides student housing and co-living accommodation and is backed by Alpha Wave, Matrix Partners and Accel, clocked ₹442 crore in revenue from operations in 2022-23, compared to ₹115 crore in 2021-22. It posted a loss of ₹495 crore in 2022-23 compared to ₹417 crore in the preceding year.

The rental housing sector in general saw an all-time peak in prices in the last two years, as demand returned and ready supply was limited.

Now, with many new players coming in and existing operators exploring more viable business models and profitability, the co-living sector may also have an opportunity to reinvent itself. Will it work this time around?

What went down

View Full Image

India’s rental housing market has mostly been fragmented and unorganized. The build-to-rent model, which worked well globally in many countries, hadn’t even scratched the surface here. It was a market ripe for disruption. Between 2015 and 2018, a slew of startups came in, offering young adults and millennials shared living spaces. The slightly higher rents and low-deposit model worked well, and they were far better in look and feel than paying guest facilities.

There was good demand, investments came in at high valuations, and the sector was poised to create a new real estate rental asset class. Flush with funds, the startups grew too fast and too soon, spreading themselves thin by scaling to multiple cities.

Among the early movers, Oyo Living, the co-living vertical of Oyo Hotels & Rooms, scaled down from 2021 onwards. It gave up several properties, converted some into hotels, and currently operates only a few co-living centres. NestAway and HelloWorld faced challenges until their acquisition. Bengaluru-based Homigo, founded by three IIT-Kanpur alumni, ran into trouble after multiple tenants accused the startup of fraud and cheating.

When the pandemic hit, co-living was the worst hit among all real estate sectors. Being a high-volume, low-margin business, it became a survival issue, as funding also dried up.

_1568191516604.jpg "Stanza Living has over 70,000 beds in 24 cities.")

View Full Image

SimplyGuest, another Bengaluru-based bootstrapped co-living startup founded in 2015, shut shop in March 2021. Co-founder Mayank Pokharna says that while the startup couldn’t survive the pandemic-led challenges, the co-living business model in general was being questioned. “Acquisitions of assets happened at unreasonable costs and landlords asked for fixed rentals. When operators underwrite the risk, and then they can’t fill the beds, they won’t break even. But they had scaled so much, it was tough to reduce costs,” said Pokharna, now a co-founder of ArtofCo, a co-living consultancy.

Stanza Living has over 70,000 beds in 24 cities. It raised $220 million in equity and debt. When equity funding was drying up, Stanza raised $57 million in a debt round, but even then it had said the funding was for growth and multi-city expansion.

Acquisitions of assets happened at unreasonable costs and landlords asked for fixed rentals

—Mayank Pokharna

“Stanza acquired properties at very high costs and expanded to too many cities. Their master lease agreements with property owners were at fixed rentals and they anticipated huge demand. But in the past year, they have been trying to rationalize costs, reduce losses and streamline operations. We have to see how it pans out,” said a person familiar with the matter who didn’t want to be identified.

A Stanza spokesperson didn’t respond to Mint’s queries.

The good news for the sector is that demand has been strong since the beginning of 2023. The shake-up has led to consolidation and acquisitions.

The learning curve

and Kalpesh Mehta.")

View Full Image

For three months last year, Gurugram-headquartered managed-accommodation platform Housr decided to pause its expansion plans, relook at its inventory, surrender a few non-performing properties, and cut losses.

After launching in October 2018, Housr, which has a co-living vertical for singles and Housr Homes for young couples and small families, primarily operated centres that were mid-income properties. Post covid, the startup tweaked its strategy and started looking at very premium properties.

With many operators fighting for survival in the post-covid era, Housr acquired Bengaluru-based co-living company Stayabode in 2022 to enter the southern market. Currently operational in Gurugram, Hyderabad, Bengaluru, Pune and Vizag, it is soon launching in Chennai and Ahmedabad.

“We have carved a niche and want to operate super-premium properties, and the demand is huge. Earlier, everyone was focusing on the number of beds and offered budget-conscious low-quality inventory, similar to paying guest or hostel accommodation. There was also no focus on the bottomline and they blew up a lot of money,” said Housr founder and chief executive Deepak Anand.

In Gurugram, for instance, its co-living facilities charge between ₹35,000- ₹70,000 per month for single rooms with food. Housr Homes, which offers fully-furnished serviced apartments, would typically charge ₹75,000 for a one bedroom-hall-kitchen.

Good-quality supply meant for rental housing or co-living is a challenge.

—Suresh Rangarajan

So far, most co-living startups have largely leased regular buildings from owners, repurposed them for co-living and then leased them to multiple tenants. Now, companies are trying to create differentiated properties that are built for the sole purpose of co-living or renting.

“The strategy has to be supply-focused because the demand is there. Good-quality supply meant for rental housing or co-living is a challenge. That prevented businesses like ours from taking off,” said Suresh Rangarajan, founder and CEO of Colive, which was launched in 2017.

In 2023, Colive launched PropEx, an online marketplace that helps user buy or rent properties that are meant only for rental housing. PropEx and Colive would collaborate with a developer for a particular building, in which the developer can sell the units to individual investors. The PropEx platform would help in selling the units, and once sold, investors would give them on rent to Colive, which would lease them to tenants, manage the property, and earn a share of the rent.

Many co-living operators are moving towards a hybrid hospitality model, which is a mix of a hotel and a rental stay.

Pokharna said that many co-living operators are moving towards a hybrid hospitality model, which is a mix of a hotel and a rental stay, offering both short-term and long-term stays. The larger focus now, however, is on growth in a sustainable manner, without burning too much cash.

Both HelloWorld and NestAway, for instance, have moved away from a top heavy verticalized structure to a flat structure with a portfolio management approach. Post acquisition, the sourcing of real estate, acquisition and onboarding of tenants is tech-enabled, with acquisition teams using data analytics for rent proposals to landlords and property owners. This basically means that at the land stage itself, the company can forecast the kind of rentals it can generate from a proposed property, the pace at which it can be filled up, and the kind of returns it can generate.

NestAway has also moved from lease and sub-lease to a service agreement model, where the risk of vacancy is reduced.

New strategies

View Full Image

Co-living platform ZoloStays recently tied up with AxisRooms, a hotel distribution technology provider, where it will use some of its empty or unoccupied rooms for short stays of one-two days. Normally, under co-living, it has to be a minimum one-month stay.

Founded in 2015, Zolostays, which also provides student housing, has a co-living investment platform, Zeassetz, like Colive’s PropEx. Last year, Zeassetz helped sell about ₹300 crore of apartments on behalf of developers to investors in co-living facilities with the promise of assured rentals. Zolo manages the properties and leases them to tenants.

“We have reduced our losses, and post covid, while we are growing, the pace of growth has become more rational,” said Nikhil Sikri, CEO and co-founder, Zolo. The company also plans to raise a fresh round of funding.

For Guesture, which operates around 3,500 beds in two properties in Bengaluru’s tech corridor Electronics City, expansion has been slow since it was launched in 2014. It has signed two properties under the built-to-suit model in another tech hub, Whitefield, which will be ready in two years. Once built, the two co-living properties would have 5,000 beds or so. Several challenges still remain. Guesture founder Sriram Chitturi says it is difficult to compete with the unorganized rental housing segment on both pricing and the facility offered.

Co-living facilities that typically offer over 150-200 sq. ft of space per person or per bed are competing with those who give 40 sq. ft per person in a paying guest accommodation. Co-living players have to charge 18% goods and services tax (GST) above the monthly rent, while unorganized operators don’t need to charge any GST.

“Co-living being a new alternative asset class has not seen large investments from developers due to the lack of demand from buyers. The buy-to-rent model is still evolving here. Once SM Reits (small and medium real estate investment trusts) buy such rent-yielding assets, post completion, a major challenge for enabling supply of efficient co-living inventory will be solved,” Chitturi said.

New kids on the block

Many startups have entered the rental housing space, offering a range of solutions that vary from co-living and student housing to more niche facilities.

Nomadgao, which operates co-working and co-living spaces in Goa and Dharamshala, targets remote workers and the digital nomad community. It plans to open up another property in Lonavala.

Settl, which launched in mid-2020, raised ₹10 crore from investors, including Zerodha co-founder Nikhil Kamath-backed venture capital fund Gruhas and We Founder Circle this year, when funding has been sparse.

The newer operators are more focused and cautious. “There have been more failures than success stories, and we are cognizant of that. We want to grow steadily, and instead of entering too many markets, we want to go deeper into each city. We have 4,000 beds and want to reach 8,000 beds by 2024-25. We are not chasing mad growth,” said Abhishek Tripathi, co-founder, Settl.

Another player, Union Living, which became operational in 2021, said it has focused on Mumbai and Pune given the huge market potential. Now, it’s planning a built-to-suit facility in GIFT City, Ahmedabad, and is also exploring Jaipur and Delhi.

Yello! Living, another new entrant, recently unveiled its first co-living facility in Whitefield, to tap into the tech professional tenant base.

“There is increased awareness of the mistakes made in the past. Operators are exploring different kinds of business strategies, and figuring out what is working and what isn’t. There is huge demand for such facilities, so we expect the sector to only grow from here on,” said Pokharna.