To assess this, the analysis used interest coverage ratio (ICR), or the ratio between operating profit and interest outgo: if the former exceeds the latter, a company has sufficient cover for its interest obligations. Companies for which the ratio was less than one were classified as ‘stressed’. (The analysis excluded India Ratings, where ICR is not relevant due to different accounting methods.)

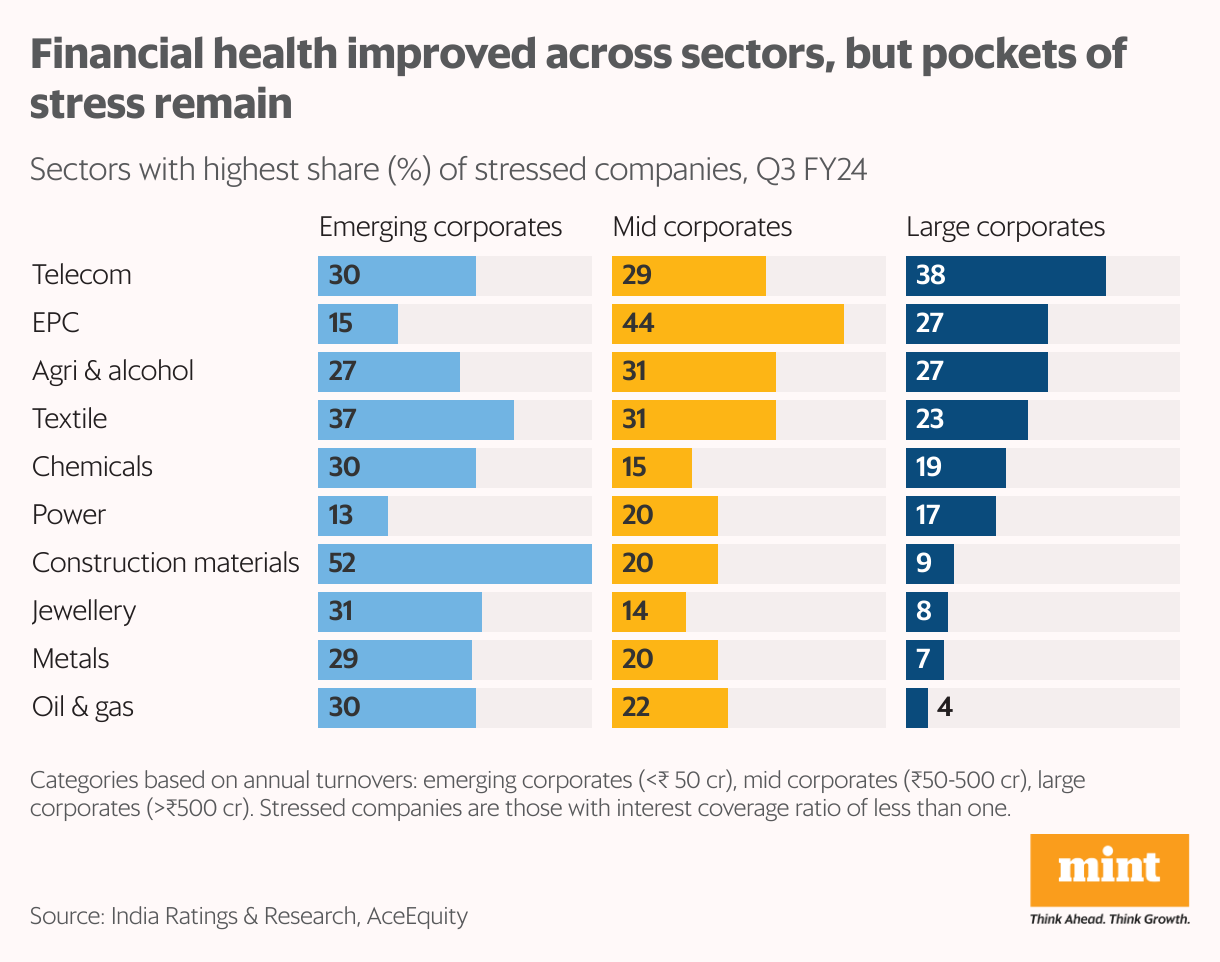

Around 12% of large businesses (annual revenue over ₹500 crore) were found to be stressed in the December-ended quarter, down from a peak of 39% in Q1 FY21. Among mid-sized businesses (revenue ₹50-500 crore), the share improved from 47% in Q1 FY21 to 20%, while for emerging ones (revenue less than ₹50 crore), it fell from 44% to 28%, the analysis found.

Upward trajectory

Based on these numbers, the study observed that mid-sized corporates had reduced their wide gap with large ones since the start of the pandemic, while smaller and more financially fragile businesses had struggled with a flatter recovery trend due to limited operating leverage and financial flexibility.

Abhishek Bhattacharya, senior director and head of large corporate ratings at India Ratings and Research, and the author of the study, attributed the recovery of mid-sized companies in sectors such as auto ancillaries, metals, and power to more nimbleness in their respective supply chains. “They are re-aligning themselves better to the end customer’s product requirement and have started to become more efficient on their own working capital management,” he said.

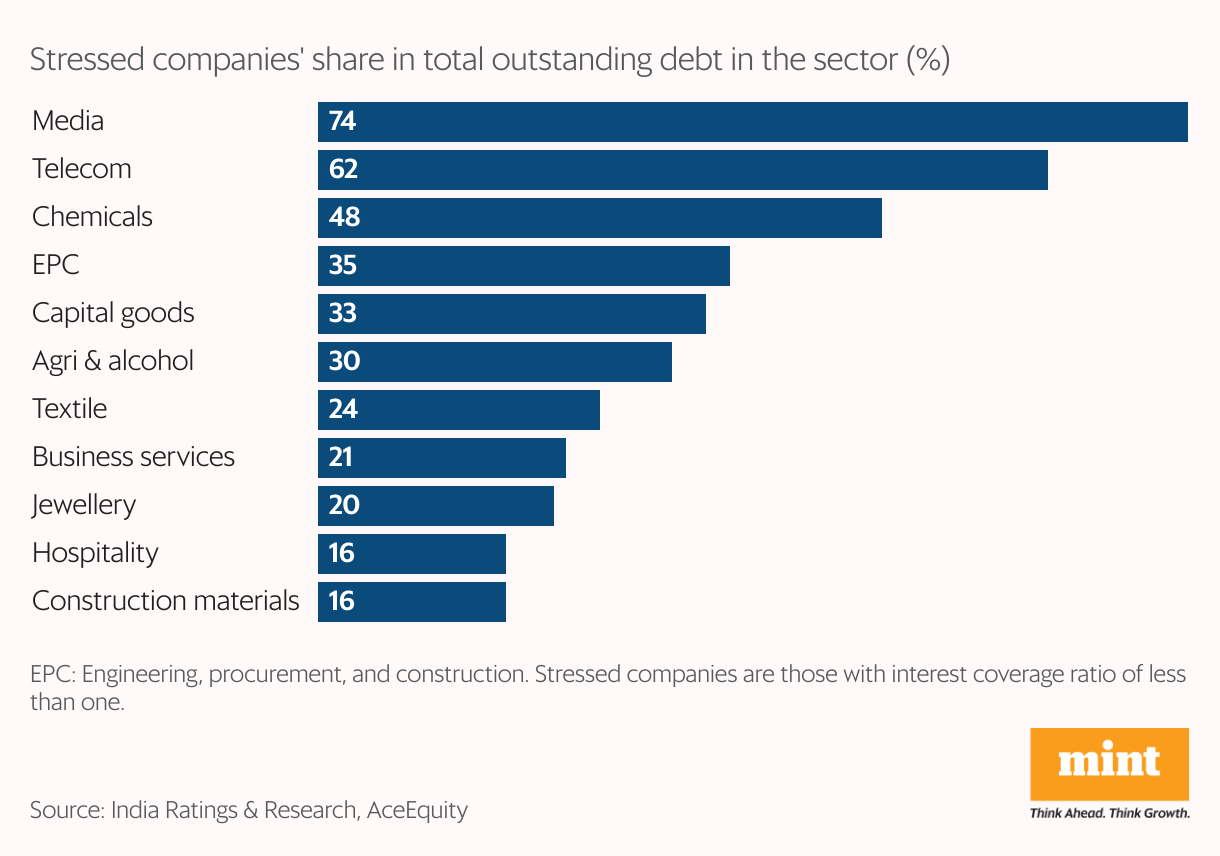

Another metric that showed recovery was the debt of companies classified as stressed. They had about 17% share in the total debt of the companies covered in the analysis, down from about 30% share in Q1 FY21. Some debt-heavy sectors—such as oil and gas, power, metals, and auto—seemed to be back in the pink of health, with this figure being less than 5–7% each, the study said. Smaller businesses exposed to lower-income segments, including bicycle part suppliers, local cement and ceramic players, and small-time ornament makers, showed higher stress.

Green shoots

Indian corporates were on a deleveraging spree in the low interest rate regime of the pandemic years, with debt-heavy sectors such as metals, logistics, power, and oil and gas aggressively switching to the balance sheet repair mode. This has stood them in good stead: for some, the share of stressed companies dropped to 15–20%, and for large businesses in these sectors, it declined to just 4–5% (from about 32% earlier in Q1 FY21), the analysis found.

These improved balance sheets are also the ones most likely to drive capital expenditure in near term and provide momentum to India’s infrastructure push, Bhattacharya said.

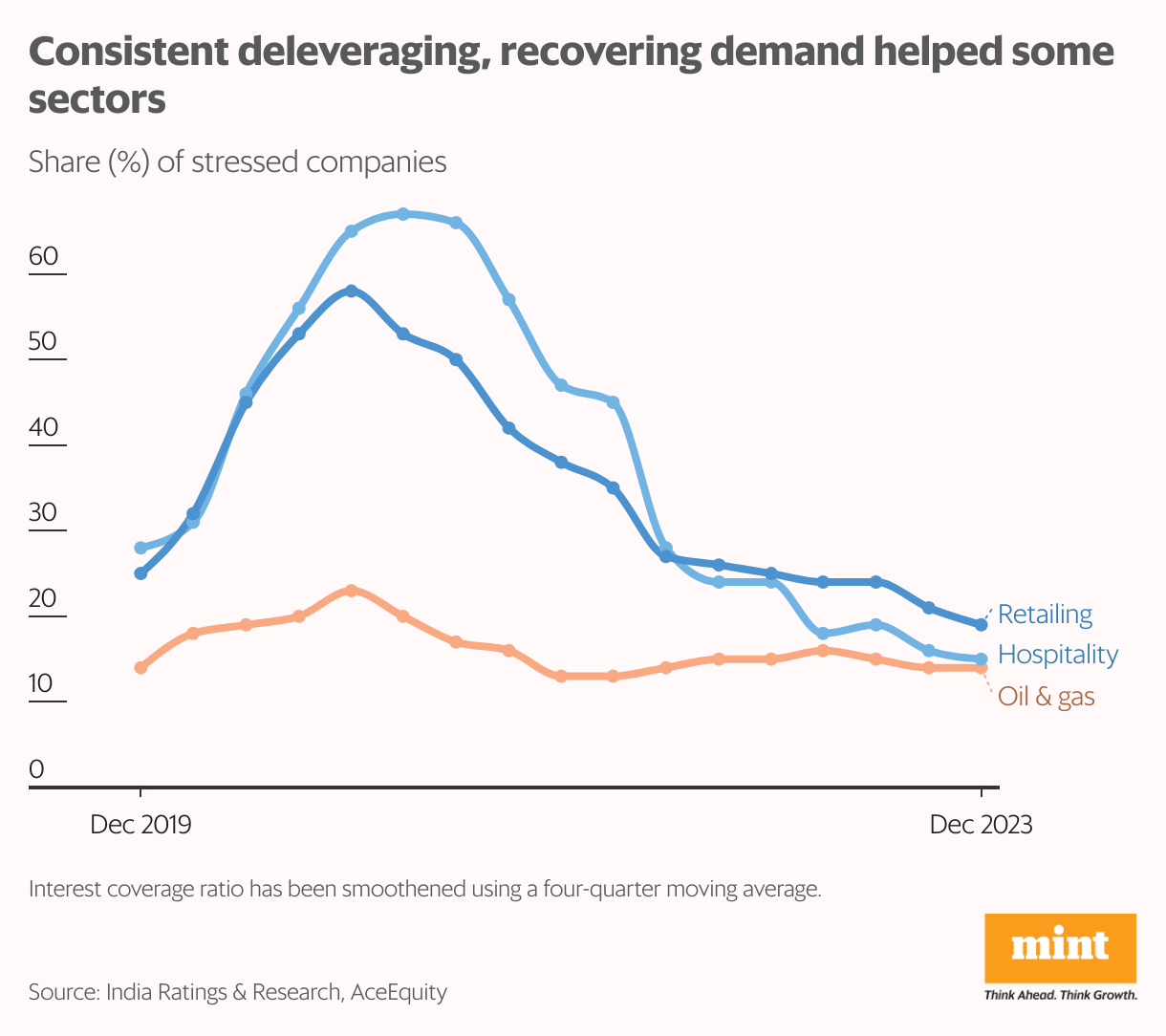

Meanwhile, there are notable signs of recovery in sectors that rely on consumption demand. Retailing and hospitality, which bore the brunt of reduced discretionary demand during covid, have made a very sharp recovery, as the share of stressed firms has drastically come off their peaks. However, at the bottom of the pyramid, the resilience of demand recovery is still under question, and is awaiting a broad-based recovery to sustain the momentum, Bhattacharya said.

Pockets of stress

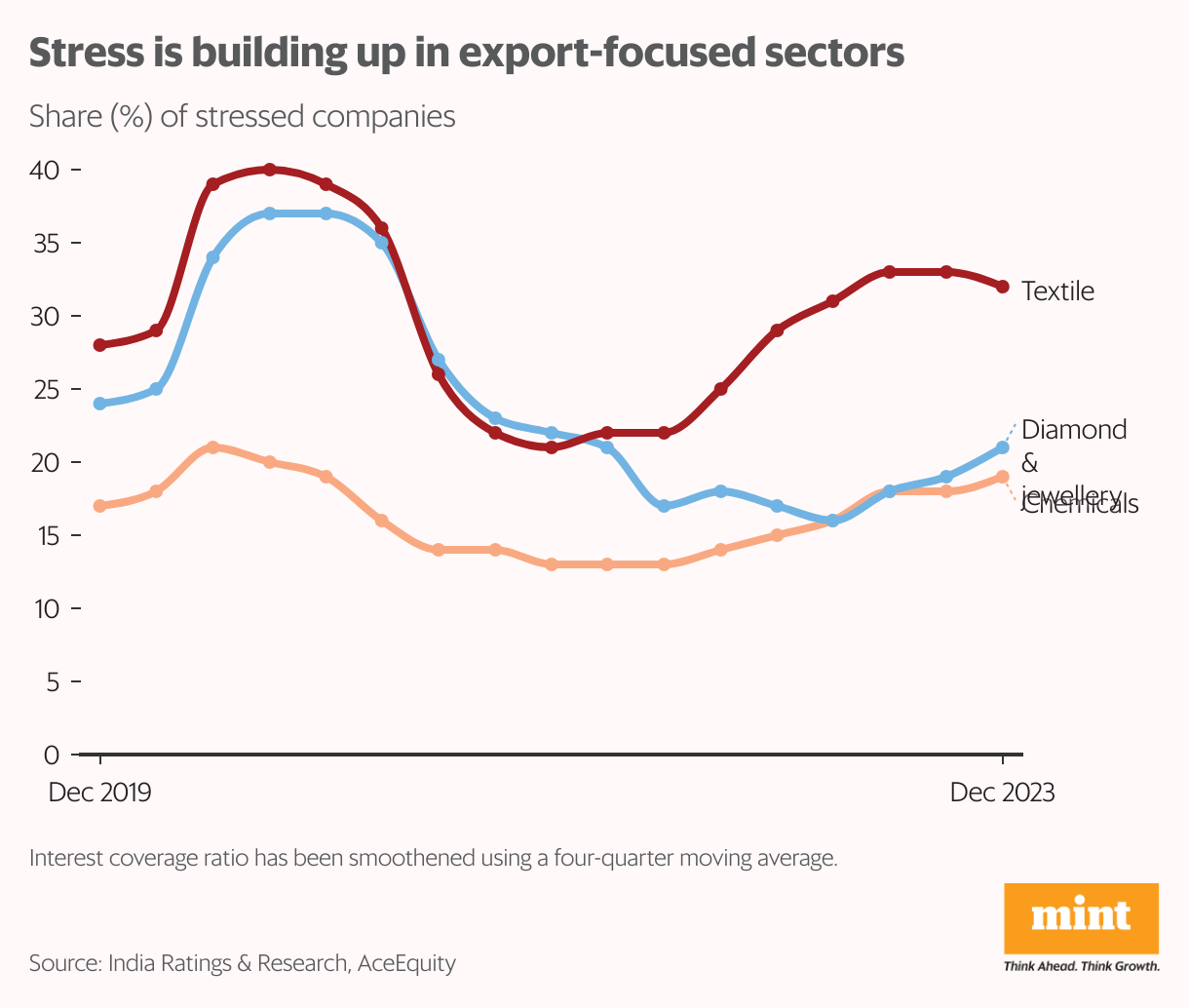

The study observed a build-up of stress in export-centric sectors, with the world going through macroeconomic and geopolitical turmoil. This trend was fairly pronounced for textiles, chemicals and the diamond industries. A recent rise in freight costs due to the Red Sea crisis could pose further risks. “A select few sectors will see stress on account of freight cost build-up,” said Bhattacharya, adding that some export-oriented sectors were already showing signs of increased stress and would be more severely impacted.

Other segments with persistently high stress despite some recent improvement included telecom and engineering, procurement, and construction (EPC), with around 39% and 33% firms, respectively, having an ICR below one. While telecom’s pain is concentrated across a few known names, EPC has taken the brunt of a liquidity squeeze and higher competition over the last few years, the study said.

A trend reversal?

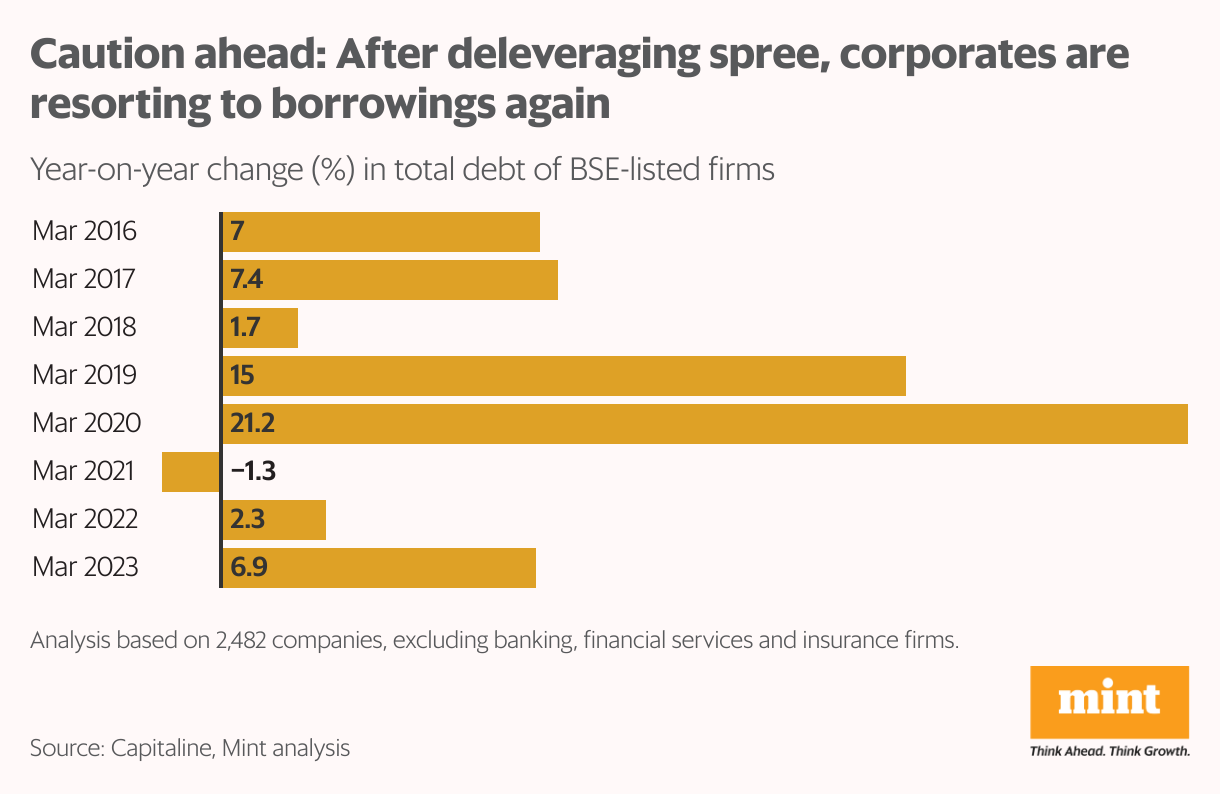

Apart from a cost overhang, a rising debt burden also raises concerns. After cutting on debt, companies have again resorted to borrowings to fund their growing working capital needs. AMint analysis of 2,482 firms, excluding banking, financial services and insurance firms, showed a 7% rise in gross debt by the end of fiscal year 2022-23, against a 2.3% increase in the previous year.

Moreover, a possible revival in private capex after the upcoming Lok Sabha elections could further boost credit demand. Bhattacharya pointed out that de- leveraging has given a lot of headroom to many infrastructure-focused sectors such as steel, power, and logistics to invest, and capex will continue there. “Yet, a broad-based capex recovery might still be some time away as corporates will continue to assess the sustainability of demand at the bottom of the pyramid,” he said, warning that fresh capex would again start leading to a build-up in leverage going forward.