On the heels of the JSW Group in 2019 and Pidilite in 2023, the Aditya Birla Group has entered the paints business through group flagship Grasim and brand Birla Opus. Tellingly, this is the group’s first major diversification foray in about 15 years. It plans to invest ₹10,000 crore and, by its estimates, add about 40% to industry capacity. Even as stocks of major paint companies took a hit in recent days, their long-term trajectory explains this beeline to get into the business.

Since March 2015, an index of paint stocks has delivered a compounded annual return of 16%, against 11% delivered by the Sensex. This is despite the price-earnings ratio of paint stocks being well ahead of the Sensex, thus being more expensive.

The new players say this is an expanding industry. Announcing its foray late last year, the Aditya Birla Group said: “The paints industry is witnessing double-digit growth year-on-year driven by rising consumer aspirations and the government’s push towards ‘housing for all’.” JSW Paints has a revenue target of ₹2,000 crore for 2023-24.

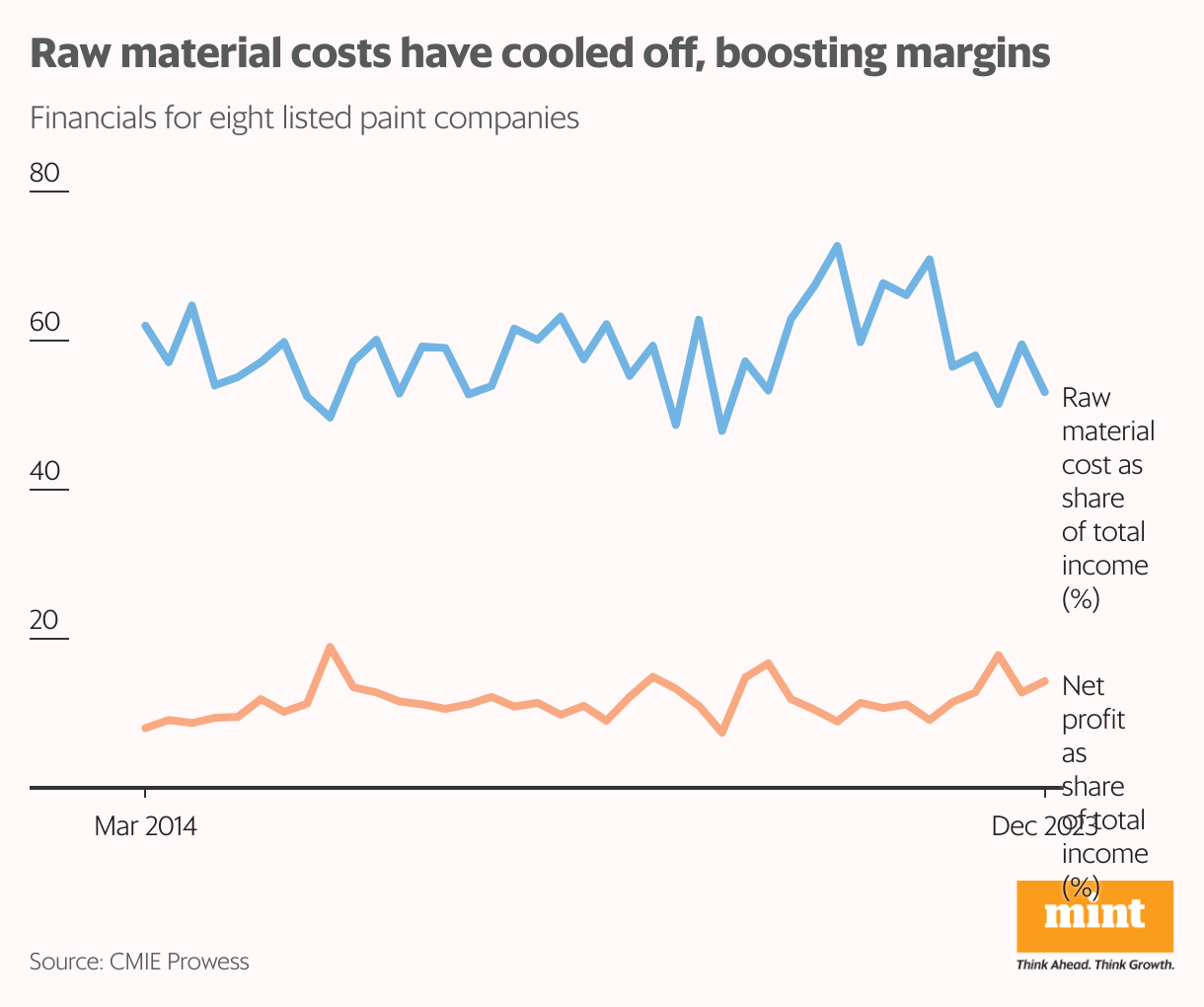

Like most other industries, the paints sector saw a major bump after the pandemic, with net sales growing 63% between 2019-20 and 2022-23. However, higher raw material costs for much of 2021 and 2022 pulled down net profit margin, which ranged between 8.9% and 11.9% in these two years for the set of listed paints companies. This forced market leaders such as Asian Paints to raise prices. In the December 2023 quarter, net margin rebounded to 14.3%, against 11.5% a year ago.

The incumbents

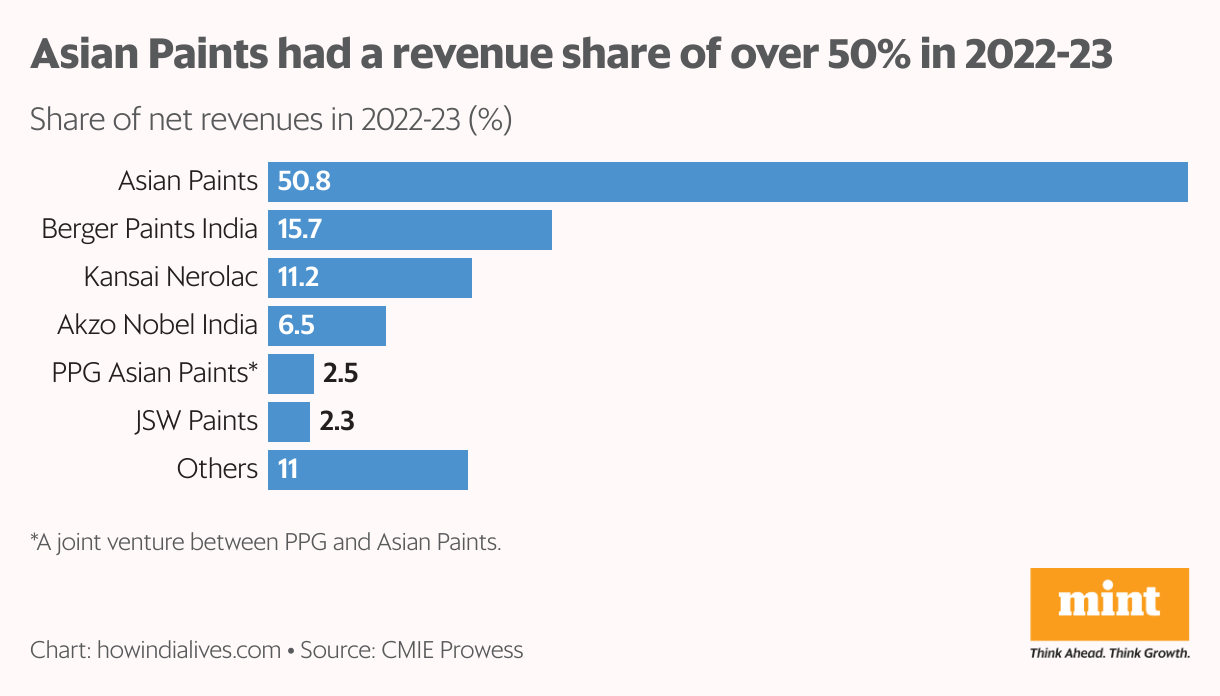

In 2022-23, the paints industry in India recorded revenues of about ₹70,000 crore. The dominant player was Asian Paints, with a revenue share of about 51%. One of the 30 stocks in the Sensex, the company’s revenue share has grown by about seven percentage points in the last 10 years. Its net profit margin in 2022-23 was ahead of the industry average by about three percentage points, and it is valued at about ₹2.73 trillion.

Then, there are Berger Paints and Kansai Nerolac, which together account for another 27% of market share by revenues. New entrant JSW Paints accounted for 2% of net sales in 2022-23. Grasim wants to be the second-largest player in the paints sector in the next few years. Even as they pump in capital into the business, new entrants have their work cut out in terms of extracting market share from industry leaders, especially Asian Paints.

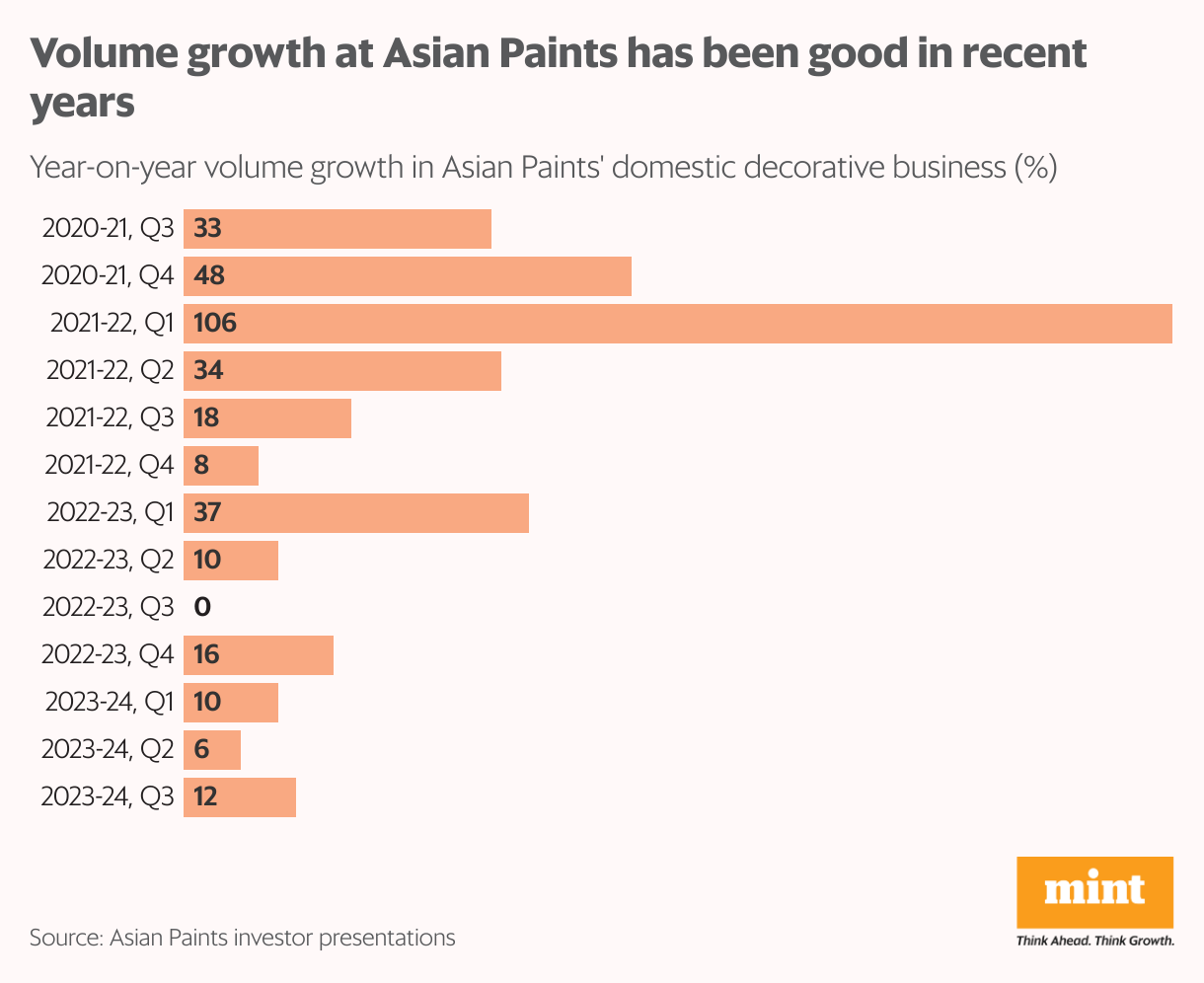

Volume growth

Market leader Asian Paints saw a major bump in both value and volume growth in the post-covid period as lockdowns eased, though the pace of growth has softened. The company’s domestic decorative paints vertical, which accounts for a bulk of its overall sales, saw year-on-year volume growth exceed 10% in 10 of the last 13 quarters. In 2023-24, its volume growth is in the 6-12% band, despite major price hikes. Growth in the third quarter was driven by a strong Diwali festive season.

In a presentation to investors for the December quarter, Asian Paints highlighted recovery in rural markets. It also said that both rural and urban centres had posted double-digit growth over the last four years. The company sees new real estate construction and the 49% increase in government allocation for the flagship housing scheme in 2024-25 as growth drivers, which will expand the overall industry. That’s what the new players are also looking to tap into.

Housing uptick

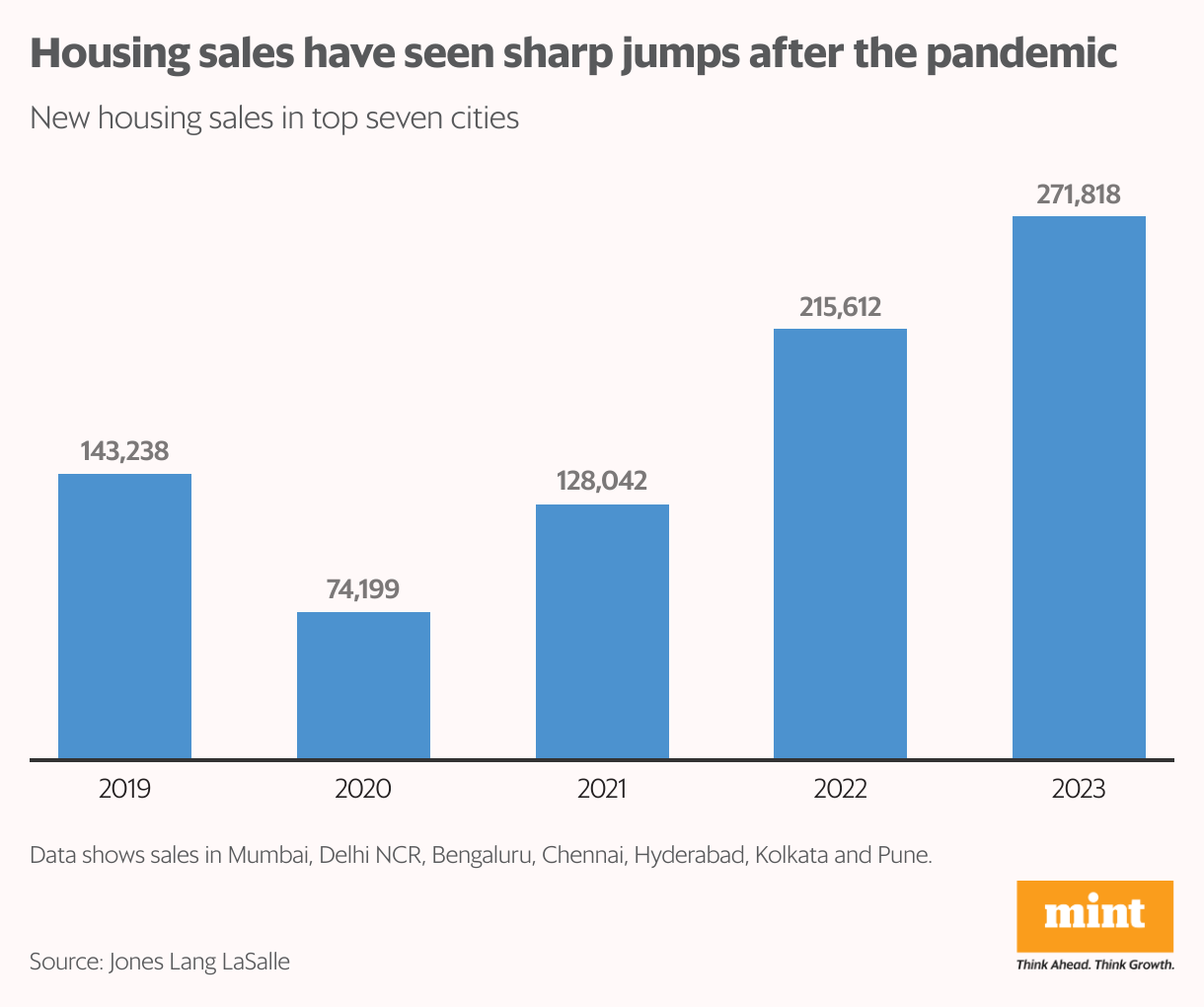

While the government flagship scheme operates at the lower end of the residential housing market, much is happening in the middle and top end also. According to real estate consultancy Jones Lang LaSalle (JLL), 2023 saw “record-breaking sales”, with about 271,900 units sold in the top seven metros. Further, residential launches in 2023 were the highest ever, surpassing 2010.

JLL expects residential sales in 2024 to be around 300,000-315,000 units, assuming interest rates decline, inflation remains moderate and GDP growth remains strong. Further, residential launches—a direct growth driver for the paints industry—are expected to grow 9-10% to 315,000-320,000 units. “Strategic land acquisition at prime locations as well as along growth corridors in cities is expected to strengthen the supply inflow across cities,” JLL said. While this augurs well for new players like Birla, the competitive fight will be interesting to see.

www.howindialives.com is a database and search engine for public data